Our problem with credit card debt

As of Q4 2024, the average Canadian owes $4,681 on credit cards, a record high. More than half of Canadians carry a balance every single month.

The problem is not easing. Credit card balances grew 9.2% year over year in 2024, reaching $124 billion for the first time. Total consumer debt in Canada hit $2.5 trillion.

Source: TransUnion Canada – Q4 2024 Credit Industry Insights Report

Millennials and Gen Z hold about 45% of Canada’s total household debt, roughly $1.1 trillion in outstanding balances. Canadians under 36 now post a 90-day-plus delinquency rate of 2.35%, nearly 20% higher than a year ago.

Source: TransUnion Canada and Equifax Canada

Money is the leading source of stress in Canada, ahead of work, relationships and health. As of 2025, 42% of Canadians rank money as their top stressor, and 49% have lost sleep over financial worries.

Source: FP Canada – 2025 Financial Stress Index

Do I need help with credit card debt?

You don’t need to be on the brink of bankruptcy to get help.

You probably need debt relief if you only make minimum payments because money is tight, use one credit card to pay off another, or avoid checking your balance because it feels overwhelming. You’re probably feeling stressed, anxious or guilty about the debt.

As of Q1 2025, 1.4 million Canadians missed at least one credit payment. That is one in 22 people.

Source: Equifax Canada – Q1 2025 Market Pulse Consumer Credit Trends

Your first steps to get out of credit card debt

1. Assess your financial situation

Don’t leave it to guesswork. Get the facts in front of you so you know exactly what you’re up against.

Make a list of all your credit cards. For each one, check the balance, the interest rate, the minimum monthly payment, any annual fees, your credit limit and how close you are to reaching it.

If you owe money on other debts like loan payments, payday loans, cash advances and lines of credit, list those as well. Write down the balance, interest rate, minimum payment and any fees for each one.

Next, access your free credit reports from Equifax and TransUnion. Pay attention to your credit utilization, which tells you how much of your available credit you are using. Credit utilization makes up a large part of your credit score. The lower the ratio, the better.

The more detail you have, the clearer your next steps will be.

Pay attention to your credit utilization, which tells you how much of your available credit you’re using. This alone makes up about 30 percent of your credit score (the lower the credit utilization ratio, the better).

The more detail you have, the clearer your next steps will be.

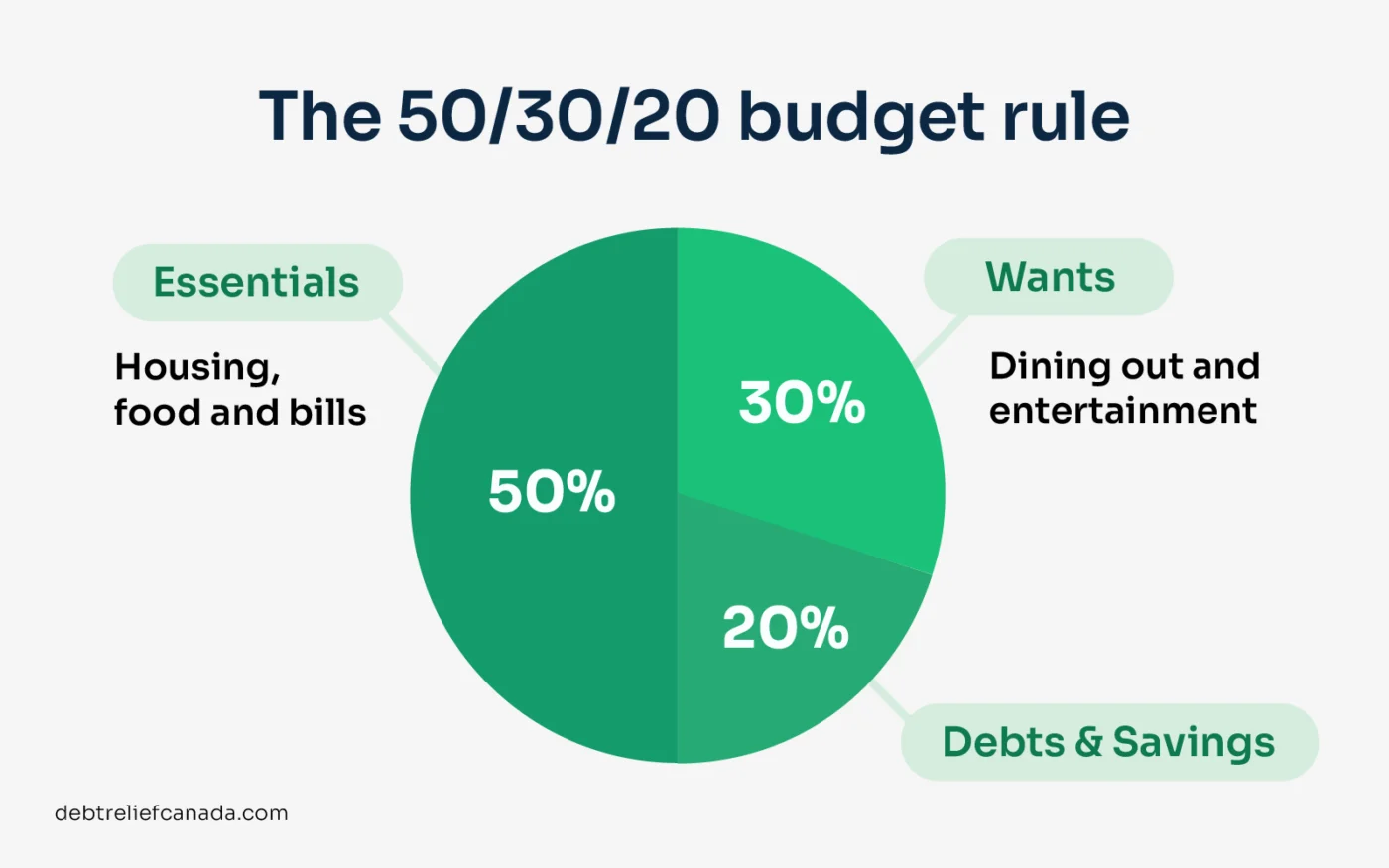

2. Work out a budget

Now, check your budget and work out exactly how much you can realistically put toward your debt each month.

The 50/30/20 rule is a good place to start: 50% for essentials, 30% for wants, and 20% for debt payments and savings.

If you’re not putting anything toward debt payments and savings, it’s time to make a change.

Once you start budgeting, you’ll find it easier to cut back on non-essentials and free up cash to tackle your debt.

A budgeting app like Goodbudget can help you see exactly where your money goes and spot areas where you can cut back.

There’s only so much you can do with your budget, but if you want to clear your debt quickly, you have to nail the basics.

Simple changes can make a big difference. Bring your lunch and make your own coffee. Cancel unused subscriptions, negotiate your bills and try a no-spend month. Sell things you don’t use and put that money straight on your debts.

3. Automate your credit card repayments

It’s all too easy to forget bills and miss payments, especially when you’re juggling debts.

Setting up pre-authorized debits or recurring payments with your credit card company ensures everything’s paid on time and avoids unnecessary fees.

Just keep an eye on your bank account and credit card statements. The credit card provider will take whatever’s due, so you need to check that the amounts are right and be careful if your income is unpredictable.

It’s also smart to add overdraft protection to your chequing account to avoid NSF fees, and set up balance alerts so you know when your balance is running low.

4. Break up with your credit card

Studies show we spend more when using credit than cash, mostly because there’s a delay between spending and paying, making it easier to ignore the true cost.

Credit card debt can sneak up on you and be tough to shift, so the best move is to stop using your cards altogether.

By cutting them out, you’ll start breaking the cycle, lower your balance on your credit cards and see your credit score improve as you do so.

Ways to get out of credit card debt

1. Debt avalanche method

To pay off your credit card debt faster and save on interest, use the debt avalanche method.

Focus on the debt with the highest interest rate first. Put all your extra money toward that one while making minimum payments on the rest.

When you’ve paid that debt, move to the next debt with the highest interest rate. Repeat this process until you have cleared your debts.

This approach saves the most on interest and clears your debts faster overall. The downside is that you will not see quick results, and if your highest interest debt is also your largest, progress feels slow at the start.

2. Debt snowball method

If you’re struggling to find motivation, the debt snowball method is worth looking at.

Don’t worry about interest rates for now. Line up your debts from the smallest balance to the largest. Attack the smallest debt first, throwing as much as you can at it while continuing to make the minimum credit card payments toward your other balances.

Once that first debt is cleared, roll the payment onto the next smallest, and keep going. It’s about building momentum and not losing steam.

You get quick wins, stay motivated and see real progress. The trade-off is that you pay more interest overall by not tackling your most expensive debt first.

3. Balance transfers

If you have a good credit score (650 or higher), a balance transfer card helps. You move your high-interest debt to a new card with 0% or low interest for 6 to 12 months, giving you time to pay it down faster.

Only use the new card to pay down debt, watch for transfer fees, pay off as much as possible before the promotional rate ends, and don’t use your old card again. Check when the promotional rate expires so you know how long you have.

4. Debt consolidation loans

A debt consolidation loan rolls multiple debts into one. You take out a personal loan at 8 to 12 percent interest and use it to pay off your credit card debt. You are left with one payment at a lower rate and a set end date.

| Debt consolidation loan | Credit cards | |

|---|---|---|

| Interest rate | 8% to 12% | 20% to 30% |

| Payment structure | Fixed monthly payment | Minimum payment (mostly interest) |

| End date | Set repayment term | No fixed end date |

| Risk | Must qualify for lower rate | Balance can grow indefinitely |

This reduces your interest and sometimes what you pay each month. But it only works if you qualify for a lower rate, so good credit is a must. You have to avoid racking up new balances, or you land yourself in double the trouble. If you use a secured loan like a HELOC and miss a payment, your home is at risk.

5. Non-profit credit counselling

If you’re struggling with debt, a credit counselling agency helps.

You can get credit counselling from both non-profit and for-profit companies, but always use an accredited, certified non-profit credit counsellor for genuine, unbiased help. Your first meeting with a certified counsellor is usually free, where you get debt advice specific to your situation.

If you go ahead, the counsellor attempts to negotiate with your creditors to reduce or freeze your interest rates, and you make just one monthly payment to the agency.

A credit counsellor typically recommends a debt management plan, and you make monthly payments to that credit counselling agency. You pay a set-up fee and a monthly fee, but the savings on interest usually make it worthwhile.

This approach is a good fit if your credit has taken a hit, but you can manage regular payments and want help staying on track.

6. Consumer proposal

If your debt is out of control, a consumer proposal is worth looking at.

A consumer proposal is a legally binding agreement, set up by a Licensed Insolvency Trustee, that lets you pay back a portion of your unsecured debt while the rest is forgiven.

You combine your debts into one affordable monthly payment, with no more interest, collection calls or wage garnishments. You keep your assets, including your home and car.

The cost is based on your income, how much you owe and what you can afford to pay. Your credit rating takes a hit, but that is far less damaging than bankruptcy, and you keep your assets.

7. Bankruptcy

Personal bankruptcy is a legal process under the Bankruptcy and Insolvency Act where you give up some assets to get help with debts you can’t manage.

Most people don’t end up here by choice. It’s often the last option for those who can’t repay what they owe. Once you declare bankruptcy, you pay what you can afford, and some assets are sold to pay your creditors.

You’re legally protected from creditors, interest is frozen, and collection action stops. When the process is done, sometimes in as little as nine months, your remaining unsecured debts are wiped out.

8. Debt settlement

Debt settlement means hiring a company to negotiate with your creditors so you can pay a lump sum that is less than what you owe.

There are big catches. Creditors don’t have to accept the deal, and you pay an upfront fee to the settlement company either way. The process takes months, and if you stop payments while they negotiate, your credit score drops.

Debt settlement companies often make promises they can’t keep and cannot stop wage garnishments, legal actions or collection calls. Don’t use debt settlement programs to file a consumer proposal or bankruptcy. These companies aren’t qualified and have no power to do so.

Only a Licensed Insolvency Trustee can give you real creditor protection in Canada through a consumer proposal or bankruptcy.

When to talk to a Licensed Insolvency Trustee

If you’re juggling cards to pay each other, if debt payments take up over 40% of your income, if you’re missing payments, getting collection calls, or if debt stress is hurting your health or relationships, it’s time to talk to a Licensed Insolvency Trustee.

Have questions about debt?

Talk to a Licensed Insolvency Trustee. It’s free and confidential.

4.8 ★ on Google 170+ reviews

What to do after paying off credit card debt

Getting out of credit card debt is a huge win, but staying debt free means keeping up the effort and sticking to good habits.

Start by setting up an emergency fund, even if it is just $1,000. This safety net helps you cover unexpected expenses without turning to credit.

Keep an eye on your budget every few months and cut out the spending habits that led to credit card debt in the first place. As you pay off your debts, start putting that money into savings or toward your future goals.

Frequently asked questions

How much credit card debt does the average Canadian have?

As of Q4 2024, the average Canadian carries $4,681 in credit card debt, according to TransUnion. Total credit card balances reached a record $124 billion.

What is the best way to pay off credit card debt?

The debt avalanche method (paying the highest interest rate first) saves the most money. The debt snowball method (paying the smallest balance first) builds motivation faster. Pick the one you will stick with.

Will a consumer proposal stop collection calls?

Yes. Once a Licensed Insolvency Trustee files a consumer proposal on your behalf, a stay of proceedings takes effect. Creditors must stop all collection calls, wage garnishments and legal action.

Does debt consolidation hurt your credit score?

A debt consolidation loan shows as a new credit account, which temporarily lowers your score. But if you make payments on time and reduce your overall credit utilization, your score will improve.

Should I use a debt settlement company?

Be careful. Debt settlement companies charge upfront fees, cannot guarantee that creditors will accept their offer and cannot stop wage garnishments or legal action. Only a Licensed Insolvency Trustee has the legal authority to file a consumer proposal or bankruptcy.

How long does credit card debt stay on my credit report?

Unpaid credit card debt stays on your credit report for six years from the date of last activity. If you file a consumer proposal, the consumer proposal is removed three years after you complete it.

Can I negotiate with credit card companies myself?

You can try. Some creditors accept lump-sum settlements or reduced interest rates if you call and explain your situation. But they are not required to agree, and you have no legal protection during the process.

What happens if I just stop paying my credit cards?

Your account goes to collections, your credit score drops, and the creditor can take legal action, including wage garnishment. Interest and fees keep piling up. Ignoring the problem makes it worse.

If you’re struggling to make your debt repayments, a free consultation with a Licensed Insolvency Trustee is a good place to start.