According to Statistics Canada, Canadians now owe $1.74 for every $1 of disposable income—a clear sign of just how stretched household finances have become.

If you’re worried about mounting debt and wondering how to reduce what you owe, chances are you’ve seen ads shouting about “government debt relief,” “government grants,” or promises of “debt forgiveness” that sound too good to be true.

Sounds good, but is it real? Sort of. Debt forgiveness is not a magic wand, but there are legal ways to reduce or even write off what you owe if you’re struggling to keep up.

We’ll walk you through what you need to know about debt forgiveness in Canada.

Key takeaways

- With debt forgiveness, debts can be written off, but only if creditors think you genuinely can’t pay.

- Most unsecured debts can be forgiven, but student loans and tax debts only qualify in specific situations.

- A consumer proposal is the most common way to get debt forgiven in Canada.

- Debt forgiveness is just one of several options available to resolve debts.

Contents

What is debt forgiveness in Canada?

Debt forgiveness is when a creditor agrees to cancel all or part of your debt, usually because you simply can’t afford to repay it.

If you’re in serious financial hardship and can’t even make the minimum repayments, some lenders may eventually decide it’s not worth chasing and write off the debt as a loss. This is especially true if you have no income or assets.

For example, if you’re unable to make even the minimum payments on a credit card debt, the lender may decide it’s not worth pursuing and may write off the balance if you have no income or assets.

But don’t expect this if you do nothing. Creditors won’t write off debt unless you take action and show you genuinely can’t pay.

Is there really a debt forgiveness program?

In Canada, there are no official government-backed debt forgiveness programs available or a government grant that just clears your debt—it doesn’t work like that.

In Canada, debt forgiveness typically happens through one of two formal debt relief options: a consumer proposal or bankruptcy.

Both are legally binding options administered by a Licensed Insolvency Trustee (LIT), a regulated insolvency professional licensed by the federal government.

They’ll handle the negotiations for you, often reducing what you owe or arranging more affordable repayments.

Not everyone qualifies, and not all debts are eligible. Let’s break down how each option works and which ones actually offer debt forgiveness.

What debt forgiveness programs are available in Canada?

The main debt forgiveness options in Canada are consumer proposals and bankruptcy. Both are legal programs that can reduce the amount you pay back.

Other options like debt management plans or consolidation loans can make payments easier, but they don’t forgive any of the debt.

| Program | Provided by | Debts covered | Debt forgiven? | Duration |

|---|---|---|---|---|

| Consumer Proposal | Licensed Insolvency Trustee | Most debts | Yes | 1-5 years |

| Bankruptcy | Licensed Insolvency Trustee | Most debts | Yes | 9-21 months (longer with income) |

| Debt Settlement | Debt settlement company | Most debts | Not typical | 2-5 years |

1. Consumer proposal

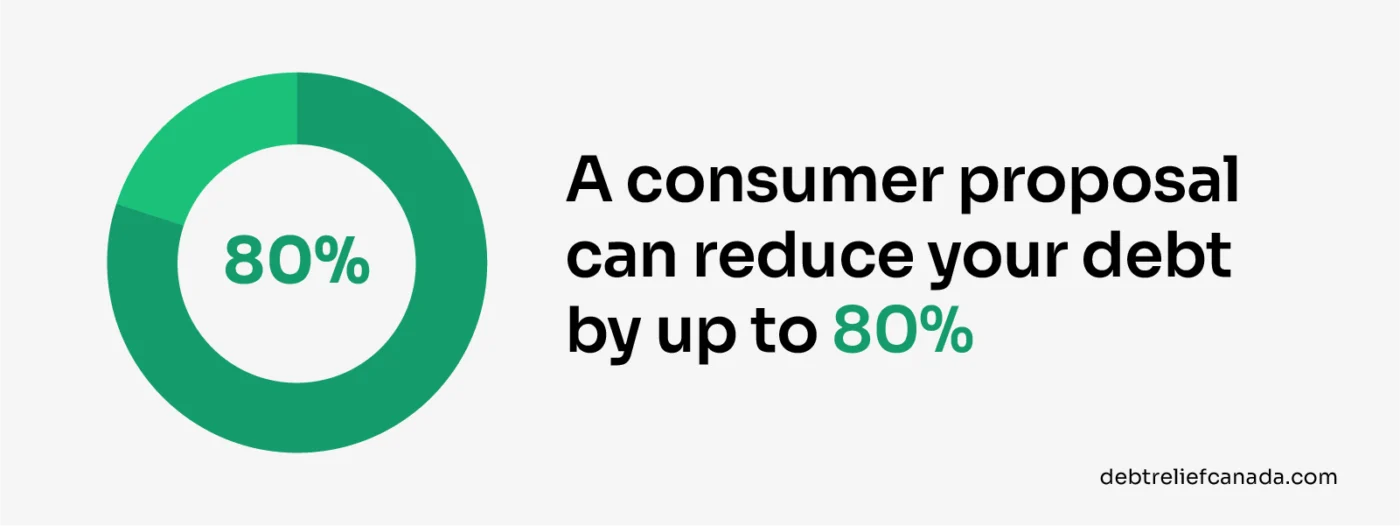

A consumer proposal is a formal, legally binding agreement between you and your creditors. It’s arranged with the help of a Licensed Insolvency Trustee. A Consumer Proposal is the most common formal path to partial debt forgiveness in Canada.

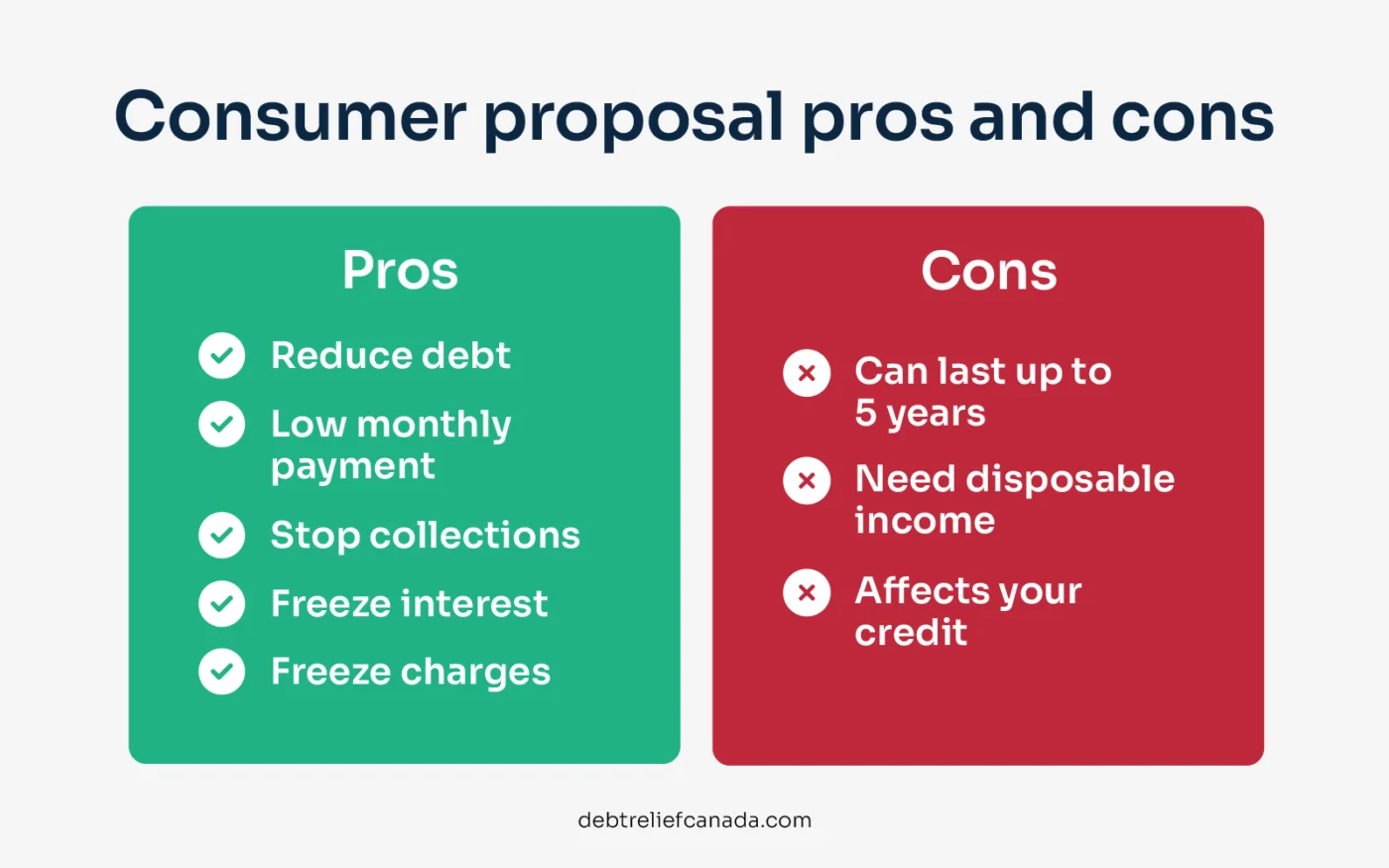

You repay a portion of your unsecured debt, often reducing what you owe by up to 80%, through fixed monthly payments for up to five years.

If you stick to the plan, interest is frozen, collection calls stop, and you’re legally protected from creditor action.

And here’s the key bit: any remaining eligible debt at the end of the proposal is forgiven, giving you a clean break, without going bankrupt.

Unlike bankruptcy, you keep your assets in a consumer proposal. There’s no requirement to give up valuables like your home or car.

The consumer proposal is the primary government debt relief program in Canada.

They’re often marketed as “government debt forgiveness programs” because they’re federally regulated and can only be arranged through a Licensed Insolvency Trustee.

They’re backed by the Bankruptcy and Insolvency Act, meaning it’s legally binding and enforceable by law.

Most unsecured debts qualify for a consumer proposal. Student loans only qualify if you’ve been out of school for 7 years or more, and CRA debt can be included if your returns are filed and they accept the offer.

A consumer proposal will impact your credit rating. It stays on your credit report for at least three years after completion, which can make borrowing more difficult in the short term.

2. Bankruptcy

Bankruptcy is a last resort to eliminate your debts.

If you qualify, you’ll face restrictions for 9–21 months. Upon completion, your unsecured debts are officially discharged.

It can be the right choice if your financial situation is severe. But declaring bankruptcy is a legal process with serious consequences, including possible loss of assets.

Your credit score will take a major hit, affecting your future ability to borrow money.

Also, not all debts are forgiven. For example, student loan debt cannot be included unless it’s been at least seven years since you left school.

3. Debt settlement

Debt settlement means negotiating with your creditors to settle your debt for less than the full amount owed. You typically offer a lump-sum payment, and if they accept, the rest of the balance is forgiven.

You don’t need a debt settlement company. You can contact creditors directly, but get any agreement in writing before handing over any money.

Creditors usually only entertain offers if you’re already behind on debt payments and they believe you’re unlikely to repay in full.

While it can lead to partial forgiveness, creditors don’t have to accept your offer.

Debt settlement is an informal arrangement with no legal protection. Creditors can still sue you, garnish wages or continue collection efforts until a deal is reached.

Be especially cautious of debt settlement companies that charge high upfront fees or promise to erase your debt quickly. Many don’t deliver, and scams are sadly common. Make sure you fully understand the fees charged by debt settlement companies before agreeing to anything.

If you’re considering debt settlement, be aware that it’s not always the safest route and isn’t a legally binding debt forgiveness program.

Speak to a Licensed Insolvency Trustee first. They can walk you through better, more reliable options.

Can student loans be forgiven in Canada?

Student loan forgiveness is available in certain circumstances, but it’s treated slightly differently than regular debt forgiveness. Here’s a quick rundown:

1. Repayment Assistance Plan (RAP)

If you earn under $40,000, you may not need to make payments. The government can cover interest and, in time, forgive the rest.

You can apply every 6 months through the NSLSC.

2. Federal forgiveness for doctors and nurses

If you are an eligible medical professional who works in underserved rural or remote areas, you may qualify for federal student loan forgiveness.

Doctors can apply for up to $60,000 of student loan debt forgiven over five years.

Nurses may be eligible for up to $30,000 in forgiveness, provided they complete at least 400 hours of in-person service each year.

3. Provincial Programs

Under the B.C. Loan Forgiveness Program, you could have the provincial portion of your Canada-B.C. integrated student loan debt forgiven at a rate of up to 20% per year for a maximum of five years. You’ll need to work in an eligible job to qualify.

Quebec’s Loan Remission Program forgives 15% of your student loan if you finish your program within a set time and receive a bursary each year through the Loans and Bursaries Program.

The Nova Scotia Student Loan Forgiveness Program can wipe out the provincial portion of your student loan, up to $20,400 over five years. You must have graduated, and your loan must have been issued on or after August 1, 2015.

If you studied in Prince Edward Island and borrowed more than $6,000 in student loans each year, you may qualify for the PEI Debt Reduction Grant. Depending on when you began your program, you could get $2,000 to $3,500 per year to reduce what you owe.

4. Consumer Proposal or Bankruptcy

Student loans can be wiped out through a consumer proposal or bankruptcy, but only if you’ve been out of school for 7 years or more. Otherwise, you will remain responsible for repayment.

Does debt forgiveness hurt your credit score?

Yes, but don’t let that put you off. Debt forgiveness will usually impact your credit score, but if you’re already behind, your credit’s likely taken the hit.

Getting back in control is often worth the trade-off, and you can rebuild your credit over time.

Here’s how long each option stays on your credit report in Canada:

| Program | Impact on credit | How long does it stay on a credit report |

|---|---|---|

| Debt Settlement | R7 | 2 years after the debts have been repaid |

| Consumer Proposal | R7 | Equifax: 3 years after completion or 6 years from the filing date (whichever comes first). TransUnion: 3 years after completion or 6 years from default. |

| Bankruptcy | R9 | First-time: 6 years after discharge (7 years in NL, ON, QC and PEI with TransUnion). Second-time: Remains on file for 14 years with both credit bureaus. |

An R7 rating means you’re repaying debts under a special arrangement. R9 is the lowest score, used for bankruptcy. But neither lasts forever.

Alternatives to debt forgiveness

These options don’t forgive your debt like a consumer proposal or bankruptcy does, but they can help you save money on interest and pay off your debt faster.

1. Credit card balance transfer

If your credit score is healthy (650 or above), a balance transfer credit card could give you a breather.

It lets you move high-interest debt onto a new card with 0% or low interest for 6–12 months. That means more of your money goes toward clearing the debt rather than the interest.

Don’t spend on the card, just focus on paying down the balance. Watch for transfer fees, which are typically 1–3%, and clear as much debt as you can before the promotional period ends.

Also, avoid running up your old credit card again, or you could end up in a worse position. Always check when the promo rate ends, or you could get stung by higher interest later.

2. Debt Management Plan via non-profit credit counselling

A Debt Management Plan (DMP) can make debt more manageable, but it’s not a debt forgiveness program.

You’re still expected to repay the full amount you owe, just in a more structured and affordable way.

You offer a payment plan to your creditors, letting you pay off your debt in monthly installments you can afford.

Set up through a non-profit credit counselling agency, a DMP combines your unsecured debts (like credit cards) into one monthly payment. Interest is often reduced or frozen, which helps stop your balances from spiralling further.

The length of the plan depends on what you can realistically afford to repay each month.

Creditors rarely offer debt forgiveness in a DMP, but it’s not completely off the table. Some creditors may agree to write off a portion of the debt, but this isn’t guaranteed.

Creditors will often agree to freeze interest and charges, making it easier to repay what you owe.

As with most debt relief programs, a Debt Management Plan will impact your credit score. It’s reported as an R7, meaning you’re repaying through a special arrangement. But as you pay down your debt, your score will start to recover.

3. Debt consolidation loan

A debt consolidation loan isn’t a debt forgiveness scheme as it won’t reduce what you owe. Its big advantage is that it can make it easier to manage multiple debts.

You take out a new loan to pay off all your existing debts, leaving you with a single monthly loan payment, often at a lower interest rate.

That money is then distributed amongst all your creditors, streamlining the debt repayment process.

It doesn’t forgive your debt, but it can simplify debt management and help you avoid missing payments or defaults.

Just be sure you can afford the new loan and avoid racking up fresh debt on cleared credit cards.

Debt consolidation may cause a small dip in your credit score at first, but if you make your payments on time, it can improve your score over time.

4. Orderly Payment of Debts (OPD) (Alberta and Nova Scotia only)

A court-approved plan that lets you repay debts over 5 years at a fixed interest rate. You repay the full amount, but it’s more manageable.

Are there tax debt forgiveness options?

Yes, but not in the way most people think.

The CRA won’t just reduce your tax debt, but they will cancel penalties and interest if you’ve had serious hardship like illness or job loss. That’s done through taxpayer relief provisions.

If you can’t afford to pay the tax itself, your best option is through a consumer proposal or bankruptcy. These are legal processes that can reduce or clear tax debt, but only if all your tax returns are filed.

If you’re feeling stuck, speak to a Licensed Insolvency Trustee. They’re the only ones who can make a formal offer to the CRA to settle what you owe.

When does a debt become forgiven?

A debt is forgiven when the creditor agrees to creditor formally agrees to write off some or all of what you owe.

In legal programs like a consumer proposal or bankruptcy, debts are forgiven once you finish the terms.

- Consumer proposal: Debt is typically cleared after 1–5 years of payments.

- Bankruptcy: First-time filers are discharged after 9–21 months.

In informal cases, debt may be considered forgiven if the creditor accepts a settlement or stops chasing it and marks it as written off. There’s no fixed timeline for that.

How do I know if my debt has been forgiven?

It’s often unclear if a debt has been forgiven, so you’ll need to confirm it directly.

If your creditor agrees to write off your debt, ask for it in writing. Until you get official confirmation, the debt may still be active.

If your debt’s been forgiven, your lender may send a notice confirming you no longer owe anything.

Check your credit report with Equifax and TransUnion to see if the account shows as “written off” or “settled.”

What if creditors are still contacting me over a forgiven debt?

If a debt has been legally forgiven through a consumer proposal or bankruptcy, creditors shouldn’t be contacting you.

Make sure the debt was included in your proposal or bankruptcy, and you’ve finished your payments, then ask the creditor for a letter confirming it’s cleared.

If creditors persist, tell them the debt’s been settled and ask them to stop. If they don’t, report it to the Financial Consumer Agency of Canada or speak to your Licensed Insolvency Trustee.

How can I be forgiven of debt?

Debt forgiveness might be an option, but how do you know if you qualify?

We help Canadians find the right debt relief option, whether that means paying back what you can afford or legally writing off what you can’t.

If you’re looking into debt forgiveness or want to explore your options, call us today at 877-375-6558.